SMM News on June 17:

The overall trend of the polysilicon market has been slightly weak recently. In addition to the weak downstream market conditions, the main factors affecting polysilicon enterprises are their operating rates and inventory pressure, which have become the primary contradictions in the market. Against this backdrop, before the SNEC exhibition, there were frequent and varied rumors about production resumptions/suspensions at different polysilicon bases, mainly involving Sichuan, Xinjiang, and Inner Mongolia.

With the opening of the annual exhibition, market participants had the opportunity to gather and exchange information. Several polysilicon enterprises also came forward to discuss their own operating status and the healthy development of the industry, providing the market with some official news.

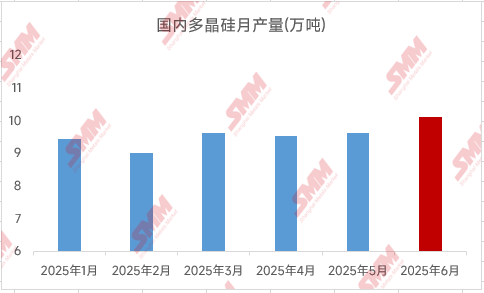

Currently, the domestic polysilicon production in June is relatively certain, with most enterprises maintaining their original plans for production starts and stops. It is expected that domestic production will reach a level of around 100,000 mt.

However, uncertainties have significantly increased for July and beyond. For Sichuan, the supply volume is relatively certain, with an expected monthly supply of 15,000-19,000 mt during the rainy season. But for Inner Mongolia and Xinjiang, they will become the main variables affecting market changes. The attitudes of key enterprises will also influence the recent and even H2 trends of the polysilicon market to a certain extent.

According to SMM data statistics, the current operational or conditionally short-term resumable capacities in Xinjiang and Inner Mongolia are 710,000 mt and 890,000 mt, respectively. Whether some local capacities of top-tier enterprises will be completely shut down, resumed, or whether enterprises will act in unison has become the focus of the market.

It is understood that a certain enterprise also intends to shut down all its capacities in Inner Mongolia, but the specific situation will depend on the production status of other polysilicon enterprises—many are also hesitating about their own production starts and stops, paying close attention to their competitors' moves. Although some capacities in Xinjiang started production at the end of May, they have not yet entered the reduction stage in large quantities.

Currently, most plans are expected to be finalized by the month-end.

According to SMM estimates, if polysilicon enterprises can reach a consensus on production cuts within a limited time, the monthly polysilicon production is expected to fall below 80,000 mt in Q3. Faced with the current wafer production starts and downside room, the polysilicon supply and demand are expected to significantly improve in Q3, with destocking of several tens of thousands of mt or even approaching 100,000 mt not being impossible, which would be favorable for polysilicon prices at that time. However, if polysilicon enterprises take the other extreme, the monthly polysilicon production may exceed 110,000 mt or even 120,000 mt, further increasing the inventory pressure on polysilicon and potentially further compressing the enterprises' survival space.

Undoubtedly, the actions of the two top polysilicon enterprises are of particular importance, with various true or false rumors circulating in the market. We still need to wait for the official information on the actual resumption of work at polysilicon enterprises.

》Check the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)